Energy Prices, Inflation and Denial

By Euan Mearns on June 11, 2008 - (Courtesy "theOilDrum.com")

Higher energy prices are feeding through to rampant consumer energy price inflation. And yet the authorities and many investment houses still see energy prices falling in the future. This naive view of global energy supplies is starving energy markets of the capital required to expand conventional and alternative energy supplies.

UK National Grid, with responsibility for the distribution of natural gas and electricity in the UK, see flat to falling natural gas prices to 2015 and beyond. Comments welcome!

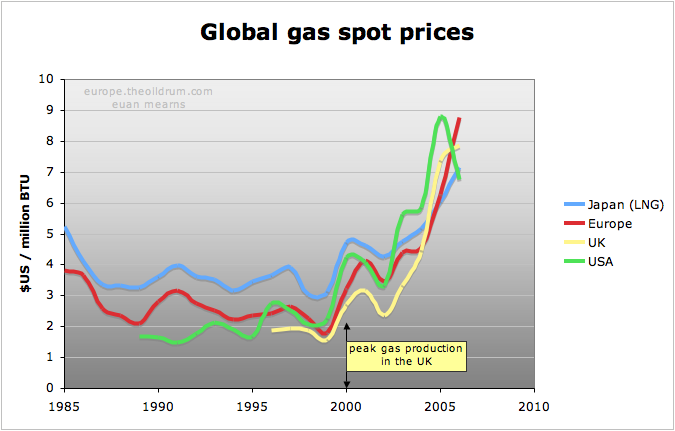

Global annual average natural gas spot prices from the BP statistical review of world energy 2007. Click all charts to enlarge

[Editor's note: this story was first run on 4th February 2008]

Global gas spot prices began their sharp up-trend around the year 2000 which just happens to coincide with the year of peak gas production in the UK. Since 2000, UK gas spot prices have increased almost 4 fold and this along with higher coal and oil prices is beginning to have a significant impact upon UK inflation.

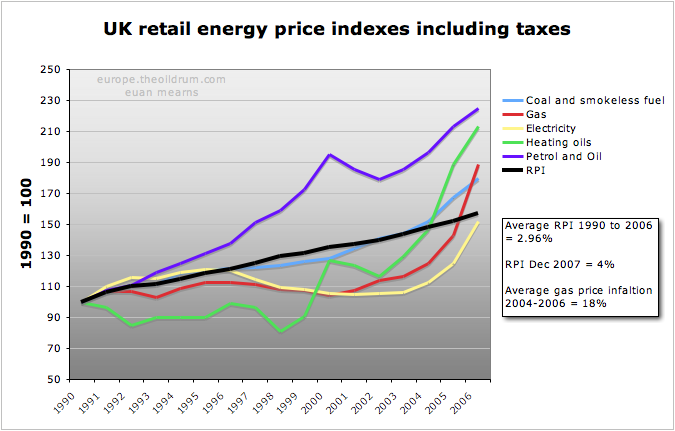

The chart is compiled from Table 2.1.1. from the report Quarterly Energy Prices December 2007 (pdf), found in the Energy Statistics section of the BERR web site. From 1990 to 2000 inflation in most primary energy sources was benign in the UK, excluding petrol (gasoline) which was deliberately inflated by progressive tax increases. Since 2003, however, inflation in gas, electricity, coal and heating oil has taken off. RPI data can be found at National Statistics Online.

Prior to 2003, price inflation in UK primary energy sources was running well below the inflation rate as measured by the RPI (the Retail Price Index is a holistic UK inflation indicator). Since 2003, inflation in all primary energy sources has taken off and for example gas prices have increased on average 18% per annum for the last three years. Prior to 2003, low energy costs had a dampening impact upon inflation but now they are running well above the RPI and this may result in inflation spreading through the UK economy since energy use impinges upon numerous goods and services.

Electricity and gas prices have just been raised significantly in the UK leading to howls of anguish from the public and the media.

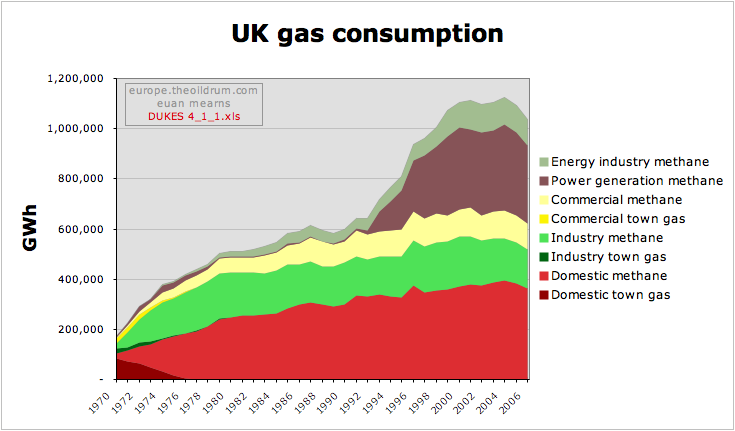

The meteoric rise in UK gas demand was reversed these last two years as amongst other factors, high price has dampened domestic demand. Data from department of Business Enterprise Regulatory Reform (BERR) table 4.1.1.

Demand for gas has fallen in the UK over the last couple of years. This may be due to a number of factors such as milder winters, efficiency measures, off-shoring energy intensive industries, switching between coal and gas in power generation and demand destruction among industrial and domestic users. Higher prices and scarcity play a role in four of these five factors.

But note, even though demand has fallen UK spot prices for gas are running about double last year.

National Grid

National Grid is a UK company with responsibility for electricity and gas distribution networks. Their web site is a goldmine of data and reports on the UK domestic energy situation. The next three charts come from their Gas Transportation 10 Year Statement 2007.

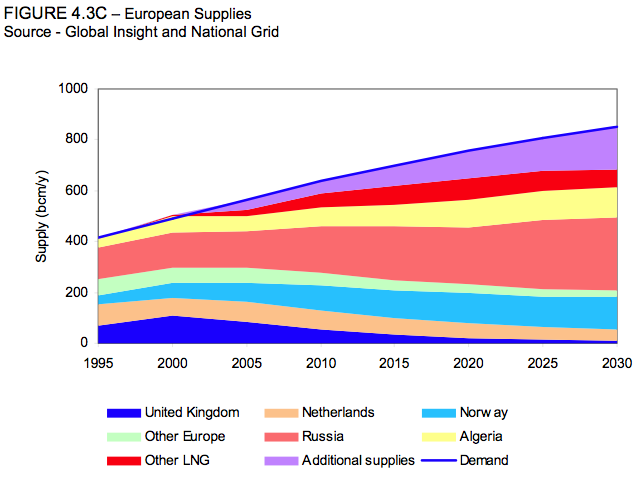

The National Grid view on UK gas supply and demand is shown below. UK domestic gas supplies are forecast to fall, demand is forecast to rise and imports will rise from zero in 2003 to 80% of total demand by 2017. This complies with my own view, and is in general agreement with the official government view expressed by BERR and is repeated in many industry reports. There seems to be unanimous agreement that UK gas imports are going to explode in the coming years.

National Grid paint a sensible picture of falling UK indigenous supply of gas, rising demand and escalating imports. And yet they forecast gas prices will fall. Source is National Grid Gas Transportation 10 Year Statement 2007

Surprising then that the National Grid has forecast gas prices to fall in 2008 and then stabilise for the next 10 years. I find it truly remarkable that a strategic company such as this can foresee a yawning gap opening between UK gas supply and demand and at the same time forecast falling to stable prices. This in my opinion sends out completely the wrong message to government, consumers and to the investment community.

Beach price is presumed to be the wholesale price. Note that this is significantly lower than the spot price since much gas is sold at contract prices struck many years ago. Industrial consumers paying the lower "Interruptible" tariff will be first to have their gas turned off when supplies fail. Note that domestic users pay by far the highest price and will be last to be disconnected.

Prices are struck in 2006 pence hence discounting future inflation which the Bank of England is mandated to hold at 2% per annum. Source is National Grid Gas Transportation 10 Year Statement 2007

Whilst UK spot prices for gas have near quadrupled since 2000 the wholesale and retail prices have risen by more modest amounts of around 50% since these are cushioned by long term gas sales contracts struck at a much lower price many years ago. These have protected UK consumers from the full glare of the gas spot market but with time this position will unravel. As old contracts and supplies expire new contracts for gas will be struck at considerably higher and rising prices. It's possible the retail prices we are seeing right now are the tip of an energy price iceberg that is preparing to rip through the system.

And yet the National Grid forecast prices to fall this year whilst UK consumers have just been hit by 15 to 20% rises.

This extraordinary view on future prices from the National Grid is rooted in their forecast for future European gas supplies which shows Russian Gas, Norwegian Gas and LNG imports expanding into the future. As I discussed in my post on The European Gas Market that was updated here, Russian gas supplies may at best maintain current levels - and not double as shown by National Grid (Global Insight report), Norwegian gas production may actually fall from 2010 onwards and LNG supplies may fall well short of the import capacity that has been and is being built.

The National Grid and Global Insight paint a rosy picture of gas supplies to Europe that does not seem to take into account falling production in Russia's largest gas fields, the reality that associated gas production from Norwegian oil fields will follow their oil production down and that Global LNG supplies will only meet around 50% of import expectations. Ironically the LNG import / export capacity offset is described in a report by Global Insight (large pdf). Source is National Grid Gas Transportation 10 Year Statement 2007

The harsh reality of this situation should be self evident from the fact that UK spot prices for gas have doubled again this year. It's really time for The National Grid, The Markets and The Government to waken up.

Denial and deprivation of investment

I mention our markets here because, since I started to follow energy markets and companies in 2003 the expectation for the future has always been that prices will fall - even though energy futures prices switched to contango.

This century, energy companies have bought back stock on an unprecedented scale whilst contemplating their corporate navels and avoiding real investment in future energy supplies. No wonder then that energy supplies are waning and prices are going through the roof.

Energy companies like BP find their stock valuations languishing at the same level of Jan 2005 and trading on a lowly PE multiple of 9 times historic earnings despite the meteoric rise in oil and gas prices over the same period. Whilst it is true they are struggling to grow production and reserves they have also done all they can to talk down future energy prices and to avoid investing in our energy future. The market is pricing in a future fall in production and oil price and terminal decline of global energy companies like BP at a time when we need these companies to display creativity, imagination and leadership.

The chart is from Yahoo. Disclaimer - I do not own any BP stock though I do invest in energy companies.

When an energy sector presides over falling production whilst forecasting prices for their product will also fall it is little wonder that their stock values are priced in the bargain basement of Global Stock markets. It is high time that the energy industries, capital markets and governments recognise that falling production and rising demand are not compatible with falling prices and that they come together to invest this profit bounty in our energy future. That future does not lie in low eroei liquid fuels like ethanol and syncrude but in solar energy, wind energy, electricity, batteries, electric transportation and global scale HVDC grids.

It is time to invest and build.

Previously on The Oil Drum

UK Gas and Electricity Prices by Chris Vernon

Natural Gas - A Tale of Two Markets by Nate Hagens

A Closer Look At Oil Futures by Nate Hagens

No comments:

Post a Comment